Figure 1: CSR puzzle

Source: Own Elaboration

Trend and prospect of Corporate Social Responsibility

Volpentesta, Jorge Roberto

Facultad de Ciencias Económicas

Universidad de Buenos Aires

Ciudad Autónoma de Buenos Aires

jorge.volpentesta@hotmail.com

Reception date: 05/18/2016 - Approval Date: 05/23/2016

ABSTRACT

In recent years it was intensified by companies the action of incorporating their strategic and operational concepts related to Corporate Social Responsibility, Sustainability and Stakeholder Theory. The confluence and interaction of the concepts of these three constructs both in doctrine and in the actions of companies generated in these very different answers, speaking on strategies, policies and shares representing idiosyncratic interpretations of each concept, showing a unique relationship between them situation that hinders the proper classification of each entrepreneur performance.

As a first objective, this bibliographic research analyzes the historical evolution of the three named concepts, examining their origins and initial ideas and their mutual interaction and interrelation. The second objective, we sought to develop an instrument that would allow a more accurate characterization of entrepreneurs socio-environmental actions on firmer foundations that denominations that companies allocated to these actions.

Based on the investigation, and adapted for this scheme Galbreath (2006), it was possible to obtain a tool to differentiate entrepreneurs socio-environmental actions based on the theory on which design their policies and actions fundamentals. Also, this instrument facilitates the ordering of the doctrinal contributions in these issues. Finally, a prospective hypothesis of the three concepts developed in research is proposed.

KEY WORDS: Corporate Social Responsibility; Sustainability; Stakeholders; Management; Company.

INTRODUCTION

Corporate social responsibility (CSR) is a concept that after more than a hundred years known at this time assumes an important role in the business world. This reality is compounded by the emergence in recent decades of sustainability and the importance attached by businesses to their stakeholders -the groups called stakeholders-, facts rewire the current actions of the companies, especially those with negotiations and social and environmental behavior.

The confluence of ideas on CSR, sustainability and stakeholders generated very different responses companies that are expressed specifically in strategies, policies and actions in which those performed idiosyncratic interpretations of each concept separately and, in turn, a unique interface between they. In addition to the fact that each company in a particular practical translation of theoretical approach to which it adheres is done, the fact remains that there are divergent definitions in the doctrine in some of the three conceptual axes analyzed. So against each individual company management that incorporates the concepts of CSR, sustainability and stakeholders, it is extremely difficult to clearly frame their practices in some of them.

In this framework of ideas this research pursued two main objectives. First, analyze the historical evolution of each of the three conceptual axes mentioned, examining its origins and initial ideas. Second, develop an instrument to facilitate the differentiation of business actions based on its theoretical foundations, beyond the names and definitions that they give their policies and actions in CSR, sustainability and stakeholders.

Also, as these concepts are mutually influenced and interrelated in their practical application in companies, a hypothesis about its future projection is formalized assuming the confluence between them will converge into a single management theory outsold socio-environmental of current conceptual boundaries. As CSR concept more historical journey in the business world, this article bases that prospective basis taking.

To make specialized research on three conceptual axes, several sources of literature were analyzed. For this, mainly published in books and scientific journals and public documents of international organizations were used. From the original idea, it follows a path search which had the chosen concepts, since they emerged to the doctrinaire consideration and to this day. Developmental grounds is only a brief expression of the material used.

The results of this research will be useful not only to analyze in more detail discrimination and actions entrepreneurs in their efforts to ascribe the aforementioned items but also the hypothesis leaves open the discussion on their joint future projection. In turn, the scheme developed facilitates the ordering and framing doctrinal contributions, which is not expressed in this presentation for exceeding the proposition of this work.

2.1 What is known or not-CSR: trend and outlook

To frame and define the scope of this article first discusses what is meant in this context by trend and outlook. Dela Spanish Language Dictionary defines in its third meaning to the term trend as "religious idea, economic, political, artistic, etc., which is oriented in a particular direction" (RAE, 2015). In the literature review and from a diachronic vision can see how CSR has been conceptualized by the doctrine and applied in enterprises; therefore, it can be analyzed if they are elements to determine the direction in this historic journey toward which it is oriented. CSR you know how and where it comes from, but where you're going? What is its future direction?

For its part, the term perspective Latin -from late perspectīvus, and this derivative perspicĕre Latin look through, watching intently the same dictionary, in its fifth sense it is defined as "point of view from which it is considered or discussed an issue" (RAE, 2015). And in his sixth sense as "vision, tighter considered in principle to reality, which is favored by observation and distant, spatially or temporally, of any fact or phenomenon” (RAE, 2015). It is interesting to reflect on the root of this word, the act of looking through, in our case, CSR, being the starting point of view from which these issues are discussed.

So if we talk about the trend and the prospect of something, it is necessary to consider, first, what is meant by that something, in this case CSR. And this is a point on which both doctrine and entrepreneurship face a complex issue. On the one hand, when the conceptual definitions and their practical application are analyzed large differences are observed concept with numerous definitions that ideas and actions that differ widely, showing a situation in which there is no consensus expressed. On the other, obvious dissimilarities are apparent in the practices and actions implemented by the companies.

And that is why a realistic way to present the current view of the theory of CSR-and its praxis is like a puzzle (Figure 1). What happens when you want to put together a puzzle? What happens is that it is easy to identify and assemble the pieces of their edges, but do not always have much idea of what happens in its center. Today and especially considering CSR, the puzzle can find different possible armed, all valid. And they respond not only to the conceptual divergence that CSR has had throughout its history, but also to the confluence of other concepts that interrelate and articulate with it. At present, both in doctrine and in its implementation by companies play within the idea of CSR jointly and interdependently, in addition to their own concepts, Sustainability and Theory of Stakeholders.

Therefore, within those edges of puzzle representative CSR today are also stakeholder management concepts and sustainability. And how and where it originates? One way to find the answer to this question is to analyze the evolution of the concept of CSR from their first enunciations and to present.

Figure 1: CSR puzzle

Source: Own Elaboration

And in that historic tour, just enter the search definitions taken note of the variety, quantity and discrepancies that those present, and little consensus on the concept exists. The brief summary of its history now tells, locates its origins in the Anglo-Saxon world of the late nineteenth century, especially in the United States.

In order to position ourselves in space and time it must be remembered that in the beginning, as Ackoff (1994 and 2000), considered machines companies lacking own purposes and whose only function was to serve their-their owners creators- in order that they themselves they could get their own objectives which consisted almost exclusively in the pursuit of profit. So that was believed and accepted that the social function and the only responsibility of business was to give their owners a certain return on their investments.

In those early years and due to the exponential growth in the number of companies, the size they were taking and the almost slave behavior on people who occupied soon broke out on them are allegations by the societies in which they acted. According to Rodriguez Fernandez (2007), the response that companies found to counter such criticism was the material, political and moral paternalism by employers-employers, both for economic reasons or calculated search for social peace as ethical and religious commitments.

So much so that the whole development of ideas on CSR during that time and until mid-twentieth century is marked by a strong inspiration -imperante in those societies-Protestant ethic, with an emphasis on doing good as the culmination of responsibility individually and in order to mitigate system failures and, as far as possible, to repair or compensate the damage caused (Carroll, 1999).

Thus, especially in the United States, paternalism is implicitly incorporated in the understanding of CSR, and this as a way to counter criticism by large companies, its enormous power, its contrary to practices the competition and its conditions close to the farm work. Thus, in those years CSR starts its development with a mark strongly oriented towards philanthropy but not driven just by companies but by their owners or owners who understood it as voluntary consideration of public social goals alongside the private economic purposes. For Bowen (1953) was the social responsibility of business and not that of their companies. In this first stage called "conventional" characterized by philanthropic and charitable actions with a strong material and moral paternalism by entrepreneurs, CSR was not only associated exclusively to them but was even dissociated activity entrepreneur: "those decisions and actions taken by employers for reasons at least partially beyond the technical signature "(Davis, 1960, p. 70) economic interest or.

He argues that the lessons of history shows that as long as business people or any other group has social power, responsibilities have to be equated with that power. This argument is known as the Iron Law of Responsibility and is expressed specifically "social responsibilities of employers must be proportionate to their social power" (Davis, K., 1960, p. 71). The society gives power and legitimacy to the company, but in the long run those who do not use that power in a way that society considers responsible, tend to lose.

Later, Davis and Blomstrom (1966) express that CSR represents a personal obligation to consider the effects of decisions and actions on the whole social system, suggesting that businessmen apply CSR when taking into account the needs and interests of others who may be affected by their business activities. This idea raises its causal nature: it is the responsibility for the decisions and actions of businessmen warning clearly that covers RS stakeholders that these decisions and actions could affect.

Over the years companies began to ask more insistently companies assume broader responsibilities extending its services to other human values, contributing more to the quality of life that the mere fact of providing goods and services. That is what the Committee for Economic Development (1971) by defining business there by public consent and its basic purpose is to serve as a constructive way to meeting the needs of society.

At one point of this development, and primarily through the contribution made by Carroll (1979), ethics the concept of CSR, which until then had been lacking in doctrinaire definitions incorporated "CSR encompasses economic expectations legal, ethical and discretionary that society has of organizations at a given point in time " (Carroll, A., 1979, p. 500).

Ethical responsibilities are represented by the rules and ethical behavior that society expects business to continue. These behaviors and practices go beyond what the law requires, and sometimes do not play in favor of the economic interests of companies. These responsibilities include factors such as equity, justice, fairness, respect for the rights of people and not harm the community. From this point of view, different social norms even if not explicitly expressed dunks in laws, unspoken rules also represent companies must meet. The floor of CSR is the fulfillment of the law on these ideas the concept that CSR is anything that companies do beyond their legal duties and commitments sits.

From these ideas the concept of CSR is incorporated as a part of corporate performance, not as an appendix but as a facet of management. Most current definitions of CSR, explicitly or implicitly, consider the ethical dimension as an integral part of the concept (Baumann, 2016; Dempsey, 2015) as well as the idea that companies are essentially relational, so that they are linked intentionally or not with their stakeholders, as it emerges from the question of the World Business Council for sustainable development [WBCSD] (2010) by establishing that CSR is a decision of companies to contribute to sustainable development, working with employees, their families and the local community as well as society as a whole, to improve their quality of life.

Through this brief history it can be seen how the concept of CSR evolved incorporating concepts that articulates its action today: sustainability and stakeholder management. But this conceptual enrichment caused by the lack of consensus on the concept warns, as expressed Votaw:

“CSR has a meaning, but does not always mean the same for everyone. For some expresses the idea of social responsibility; for others it has to do with the socially responsible behavior in the ethical sense; for some others, it refers to being "responsible" in causally; many simply identify it with charitable contributions; some relate it to the fact of having a social conscience; many others see it as simply a synonym for legitimacy in the context of belonging or being itself or valid.” (Votaw, D., 1972, p. 25)

Finally, the ISO 26000 that makes a significant contribution by linking CSR to sustainability and stakeholders, expressing this combination of concepts in his classic definition of CSR:

“The responsibility of an organization for the impacts of its decisions and activities cause in society and the environment through transparent and ethical behavior that:

- Contribute to sustainable development, including health and welfare of society;

- Take into consideration the expectations of its stakeholders;

- Compliance with applicable law and consistent with international norms of behavior;

- Is integrated throughout the organization and put into practice in their relationships.” (ISO 26000, 2010, p.4)

Despite this widespread definition, still it warns that CSR is a concept which debate does not generate greater clarity regarding its definition, leading to greater conceptual confusion that can delay the development of a consensus theory accepted by most doctrine. Like others, the concept of CSR can be a source of controversy over its definition, and this can vary depending on its use or circumstance; in situations how are you normally generates debate further clarification on the different forms of use that can have a concept.

This raises the question whether the lack of consensus that exists, whether that conceptual confusion will result in benefit of a broader debate to try to achieve greater clarification, or if the concept of CSR falls into the category of an essentially contested concept (CEC), so that finding a single definition would be unworkable. At this point it is appropriate to point out that if we talk about CSR is talking, ultimately, business management. And if it's management in companies there is no doubt when it comes to total quality, or productivity, or Just in Time system is mentioned, and when earnings, income or career development are analyzed. Regarding these terms and concepts may be a differential aspect, but companies no one has doubts about its real meaning.

But then CSR is a confusing concept or a CEC? The CEC were exposed by Gallie (1956), who defined them as evaluative concepts related to complex goods that can be described in different ways, residing in the competitive utility generate controversy; in turn, Kekes (1977) defined them as vague, ambiguous and general. The CEC refer to cases where there are multiple meanings of key terms used in a discussion about a concept. Although originally this idea was used for certain abstract, qualitative and positively considered as justice, art, morality, logic, rationality, democracy, culture and philosophy among other notions, then its use spread to all those concepts on which there are controversies and on each part in a discussion recognizes that the use grants is challenged by other party or parties, which give a different meaning.

After analyzing these features it can be concluded that CSR is an essentially contested concept rather than simply confusing or ambiguous.

And the importance of this conclusion is that if indeed CSR is a CEC, there is little chance to be accepted by all single universal definition. Each definition given highlights the key issues and gives weight to the components that are relevant to the context and situation in which it is being used. Among the doctrinaire is assumed that the concept is complex in construction, having been widely adopted in many different areas of research, applied to different forms of organization and dynamics, in line with the historical changes that society was generating, so that their definitions arise from heterogeneous needs of diverse origin: regulatory, strategic, descriptive or management.

And the importance of this conclusion is that if indeed CSR is a CEC, This categorization as a CEC determines that remain valid different conceptions that already exist and those generated in the future, which does not invalidate the fact that you refine the concept in its central aspects even incorporating other concepts, as with the theory of stakeholders and with sustainable and perfect, but understanding that can never be resolved definitively. The center of the puzzle of CSR is constantly redesign.

2.2 Beyond the concept of CSR: stakeholders

But what about the other concepts that are tributaries of CSR and, somehow, they make up with it the center of the puzzle? There are also controversial issues present, which do not always provide clarity on the issue. For example, if you take the case of stakeholders or stakeholder groups, it is observed that is also a CEC.

The concept of stakeholders is very interesting because it has undergone significant changes since its inception around late 70s of last century. One of his first definition states that it is "any group or individual who can affect or is affected by the achievement of the objectives of a corporation" (Freeman, R., 2004, p. 229). The predominant view was that of senior management and the view was that if a group of individuals could affect, or be affected by company managers then she had to worry about that group in the sense that a strategy was needed explicit to address them, in order that the company could meet its objectives.

Meanwhile Phillips et al. (2003) consider that the term stakeholder is powerful due largely to its conceptual breadth, being that means different things to different people. However, for this same reason the term received considerations that are not in the same sense as many authors and researchers who recognize that there is conceptual confusion about the term stakeholders: Sternberg (1997), Mitchell et. to the. (1997), Phillips, Freeman and Wicks (2003), Friedman and Miles (2006), Fassin (2009), Miles (2012).

Over the years the concept has evolved through numerous academic contributions, so that the last doctrinaire who devoted himself to tell their definitions was Miles (2012), that 493 scientific papers found 435 different definitions: a definition for each 1.13 items published.

Furthermore, with respect to stakeholders there are several highly controversial issues, such as: Who are the stakeholders of each company? How to identify those who are legitimate from those who are not? Do companies have formally established management mechanisms to differentiate them, listen to their demands, and select and weigh the interests to be satisfied? Do companies actually incorporate these objectives and interests in its operational and strategic management?

Even for those who do not know much about this concept existing in the collective consciousness a very close idea of what is meant when talking about sustainability or sustainable development. Specifically, a global economic system based on concepts of increased production, intensification of consumption, unlimited exploitation of natural resources and profit maximization as the sole criterion of good economic progress, which for years guided the actions of the companies forced, especially since the last 30 years of the last century, to think that such development was not sustainable. A planet with limited resources is unable to supply indefinitely inputs of a holding with these characteristics.

Paradoxically, the beginning of the development of the concept of sustainability is located in a work that never uses that term: The Limits to Growth by Meadows et al. (1972). This book arises as a result of the initiative of the Accademia dei Lincei in Rome, Italy, later known as the Club of Rome. This institution convened in 1968 to thirty scientists, educators, economists, humanists, industry and national and international staff, from 10 different countries. The call was aimed to discuss and provide solutions on the subject of the present and the future of the human species, addressing certain issues that are of concern to all people regardless of their origin and status: poverty amidst plenty, environmental degradation environment, discrediting institutions, uncontrolled urbanization, job insecurity, youth alienation, rejection of traditional values, inflation, and other social and economic singularities.

A team of MIT -Massachussets Institute of Technology-, led by Professor Dennis Meadows (1972) studied the five basic factors that determine and ultimately limit the growth on planet Earth: population, agricultural production, natural resources, production industrial and pollution. The report argues that human degradation went beyond the limits imposed should know, so that advocate the realization of multilateral efforts, posing it as the only way to set guidelines for action on a global scale and ensure they are applied. When the origin of the concept of sustainability is analyzed stresses that the role played by companies is classified as one of the factors causing the grim picture that warned; companies begin to be so exposed to public opinion in an unprecedented manner hitherto.

Since the publication of the report are developed numerous global conferences and outstanding documents that put the focus on the environment and sustainable development are made*. The socio-economic and environmental -Our Common Future Our Common Future, better known as the Brundtland Report published in 1987 by the World Commission on Environment and Development establishes for the first time more concrete definition of sustainability saying that "it is up report of humanity to make development sustainable, durable, that is, ensure that it meets the needs of the present without compromising the ability of future generations to meet their own " (ONU, 1987, p. 23).

In 1992 the concept was refined in the United Nations Conference on Environment and Development -second Earth Summit, UN, 1992 in the so-called Rio Declaration, stating that sustainability is:

economic growth for the benefit of social progress and respect for the environment.

shared social policy that drives the economy and harmoniously.

effective environmental and economic policy that promotes the rational use of resources.

After that, many more meetings and conventions followed related to the subject. But the important thing is to observe what was the initial idea of sustainability and how, from the beginning, companies as major actors involved in the concept. Subsequently, and from work Elkington (1994), the construct takes its most consensual, which is widely disseminated through social and environmental reports of companies in the format established by the Global Reporting Initiative -GRI- and it is known as the triple bottom line result or triple-triple basis of sustainability botton line line-:

Unlike what happens with CSR and stakeholders, the concept of sustainability in the doctrine has a marked consensus on its meaning, which is not verified in the concrete implementation and practical businesses do it. Although its conceptualization has a root and a development clearly identified with the environment and care, it is an interesting exercise to observe the meanings that give the concept some companies. In this sense, reading some social and environmental reports from different companies can be seen that the concept is associated with, for example, a strong balance sheet and capital discipline; geographical diversification; prudence and risk control; efficiency and cost savings; agility, employability and vitality of the workforce; building close relationships with customers; sustained growth in profitability.

These different meanings show that, on the one hand, each company is doing a particular interpretation of the concept, sometimes quite far from its original conception. And secondly, that the term sustainability is still, somehow, over used. Or, it is about valuing their use, since it is found associated with aspects that are not necessarily close to their original meaning.

2.4 CSR, sustainability and stakeholders?

At this stage of analysis, and it is having presented both CSR and their associated -stakeholders concepts and sustainability should be able to answer to the question: what is inside the puzzle? Or: what else is? At present there is no single answer, a single criterion, since these three concepts originate from different causes and different developments in business practice were traversing each other, and in that interrelated flow each took aspects of others, and his once ceded parts of his ideas. For example, CSR in its infancy spoke little or no environmental care and sustainability emerged being an eminently environmental approach it. But after this crossing, CSR assumes environmental commitments, and sustainability gains in social issues.

Until a few years ago to have a rough idea of the content of that puzzle some concepts of perturbation theory could be used. This states that in response to a question is feasible to attempt to give a preliminary response, then systematically improve this approach, paying greater attention to small details initially ignored. As poses Green (2010), in physical terms such details are called perturbations of the initial state.

This theory is widely used in the world of theoretical physics, in which the equations of most mechanical systems can not be solved exactly, so it is necessary to develop methods to obtain approximate solutions. The idea, applied to this situation is not to provide a single, clear-cut answer, but to go approaching the final idea, step by step. Especially when the answer different factors involved.

For example, a traditional application of this theory in astronomy is when you want to determine the orbit of a space body. In these cases of very large distances, for these calculations only considered gravity. For example, in the case of our solar system, the huge mass of the sun compared to that of the other members of the solar system, determined to predict the movement of the earth only its gravitational influence is considered, discarding those of the other planets because the sun is the one who has the dominant influence on the movement of the earth and the other planets. Then, if more precision is sought, they are being incorporated gravitational influences that initially were not taken into account.

But in a system with three stars similar masses that describe orbits around each other in a trinary system, in which there is no dominant gravitational position providing a rough estimate, to achieve predict the orbits of these stars can not be considered small details, but all aspects to consider are significant. And all the threads of tissue gravity are equally important and must be considered simultaneously.

For the topics discussed in this article until a few years could the perturbation theory used in order to approach towards a satisfactory answer, since the concept was more strongly CSR, revolving around the other two. And the adjustments to the various definitions of it, as previously indicated, were details that included small portions of sustainability and stakeholders. But today these last two concepts have gained ground, increasing its own gravitational force. So to try to adequately explain CSR should also consider these two concepts. It is in the presence of a system based on three in which each component struggles to be imposed on others.

What is happening today with these issues in the real world of business? Is it still the concept of gravitationally dominant CSR concepts in this system? Both in the implementation of CSR and the sustainability and stakeholder management, business practice is inclined to adopt a certain theoretical guideline, and the orientation chosen determines the conceptual extension that each company makes the theory chosen, conditioning and you determine the policies adopted in this regard. The diversity and variety of activities and actions of CSR, sustainability and stakeholder management are based on the theoretical construct that each company makes on them.

Today is when companies are investigating these issues it is that each makes an idiosyncratic interpretation of these concepts (Flammer, 2015; Frynas y Stephens, 2015; Lund-Thomsen, Lindgreen y Vanhamme, 2016). Reality shows that different companies is very common to find approaches to which they are called different way even when conceptually mean the same thing. And similar names for actions and concepts are assumed radically different. A quick conclusion to be drawn about this reality is that there is some confusion in the use of terms and concepts. However, something sharp on the horizon responsible and transparent socio-environmental efforts: the prevalence of the concept of sustainability on CSR and stakeholder management.

The interpretation that can be given the prevalence of CSR sustainability and especially also on the management of stakeholders- is that in business management concept of sustainability is much more comprehensive and crosscutting the whole company, more manageable goals, simple inclusion in business processes and easily quantifiable. A CSR will always cost integrated management and daily practice of a company. Somehow and until many years ago, for many companies CSR was time to be good. Indeed, in the brief history could be observed how in the first definitions was considered as related to the business and not directly as an activity of companies. While sustainability, which was born associated with the business viability, provides a greater menu of economic, environmental and social indicators from the predominant forms of reports in which its management results are as follows: sustainability can display clearer and quantitatively management results.

In a horizon of no more than five years back, field investigations showed that for many large companies acting in CSR was based almost exclusively on activities in the social field, appearing in most of them as the only manifestation of action CSR, pointing to a simplification of the concept to guide activities exclusively on building links with the community. And in those activities still prevailed mainly designs reflecting a scheme of power who does something for the other, often associated with a thought remediation of the weaknesses of an economic model that could not meet certain basic needs in much of the population. In essence, these companies prevailed in the original philanthropic concept. Today, most of these same companies have implemented sustainability strategies in which CSR is the chapter that deals with the relationship with the community, especially to satisfy orders it come.

This displacement of CSR in the hands of sustainability and warned from the very names of the reports with which companies report their actions in these aspects: today there are many more that Reports Sustainability Reports Social Responsibility.

Doctrinaire often enter long controversy over terms and conceptual definitions. What is undoubtedly very interesting for the scholar who participates in these discussions, it is not so much for the manager of a company that wants to incorporate into their management tooling these ideas. The truth is that while in academia definitions and concepts are discussed, companies do. Implement strategies, policies and programs. And in general, little interest them the names and definitions of what they do. Today in business management is imposing sustainability, even though within this denomination considerations CSR and stakeholder management are incorporated, as well as other elements that have no relation to any of these three concepts.

But then: how can you identify what you are doing on one or the other company? What factors and elements exist to differentiate the efforts they consider these aspects? How to tell when a company is accountable and transparent and when not? What aspects must be evaluated to determine if a company in its communications and reports showing only socio-environmental washing face or her performance is truly legitimate and ethical?

So rather than argue and argue for names and categories should be distinguished entrepreneurs performances depending on the design of their efforts and their actual actions, as well as in relation to socio-environmental impact they have. It should be able to locate businesses within parameters that indicate how each behaves in this topic.

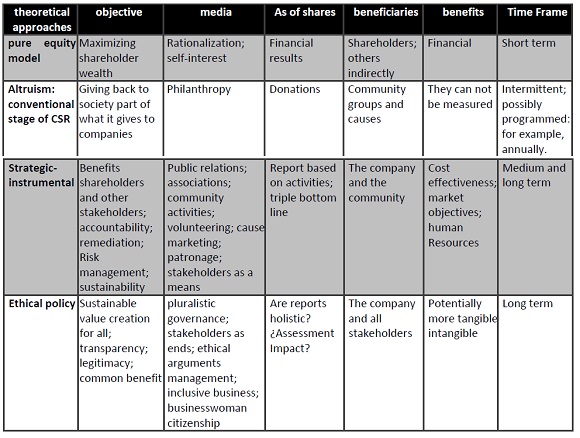

2.7 Result of interbreeding theories: by their fruits**

Many times in the life of man questions about what to do in certain situations arise: sometimes difficult to choose one path or another, to take action or another. How do you know if what you do is right? What elements must be analyzed to assess a priori about the effectiveness of a decision? This is something that man permanently delves into his own life. But also they ask managers in companies that make responsible social and environmental efforts. Moreover, from the outside look at each company, how do you identify those who perform the correct actions of which only climb to fashion to be responsible and ethical? How do you distinguish those that are genuine are wolves in sheep's clothing? How to distinguish between those companies that really have a committed and transparent performance with social and environmental development of those that do not?

Given the situation easily observable*** dispersion of names and approaches with which companies make socially and environmentally committed actions, a tool that would allow -more to put a proper name to each share- discriminate those actions on the basis of their sought theoretical foundations, contemplating the confluence and integration of the three theories analyzed.

To clearly give the names that companies provide in their communications, and be able to distinguish the most effective actions of those with lower socio-environmental impact, adaptation of a scheme Galbreath (2006) (Table 1) it was performed.

Table No. 1: Schematic adapted from Galbreath

Source: Galbreath (2006), adapted by the author

This table can display 4 theoretical foundations of actions entrepreneurs in particular and in general business conduct. For Rodriguez Fernandez (2008) in the theoretical approach of pure equity model - traditional way of conceptualizing companies- to them they are assumed as a contractual nexus within which shareholders -the principales- have primacy, exercise the right to control exclusively the board of directors and oversee the actions of managers -the agents- to prevent companies depart from the objective of creating value for them. This view companies implies a continuous search of extraordinary profits or cigars that give them higher returns to shareholders the opportunity cost or required minimum return on their investments. In pure equity model, the company should not divert resources into activities unrelated to its main objective: maximizing shareholder wealth. The evidence from research indicates that there are to be found in businesses that management under these grounds, any action of CSR, sustainability and openness towards its stakeholders.

Then, without totally abandoning the pure equity model, it has a more or less programmed or occasional conventional view of CSR made in companies through philanthropic actions voluntarily and externally, with an altruistic orientation designed to encourage being of a community. In companies that base their management on the ideas of the conventional stage of CSR actions are basically philanthropic and charitable characteristics. Actions for others, designed from a thought remediation and return to society, for all that it gives the company to operate.

Meanwhile, strategic-instrumental and ethical-regulatory approaches are the most advanced developments that provide ideas on CSR, sustainability and stakeholders, and where it is assumed that the economic objective of business is the creation and growth of wealth Total net in the long term for all stakeholders or interested parties, including the goal to compute the negative and positive externalities. For Donaldson and Dunfee (1999) this value creation, which is not only financial-and its distribution among stakeholders of companies requires the establishment of administrative schemes to resolve disputes between conflicting interests so as to achieve balance them within a cooperative scheme with negotiation.

Then, in a more advanced position than pure equity model and the conventional stage of CSR are the strategic and instrumental ideas, which as highlighted by Jensen (2002) are located in an instrumental perspective illustrated raising actions cause-related marketing, or as proposed by Porter and Kramer (2002, 2006 and 2011) through business-oriented base of the economic pyramid, or investing in a competitive or directly context through strategic philanthropy, situations all aimed at creating value for shareholders, notwithstanding which, as a result of them, some stakeholders also gain.

The strategic-instrumental to the untrained eye approach is presented with arguments that, by contrast, place it in the antipodes of pure equity approach, but in-depth analysis of their explanations can be seen how hides, subsumed, the formula of Milton Friedman (1970) but expressed more intelligently and wisely, more politically correct, considering that if the business strategies taking into account the interests of stakeholders, this generates an increase in the benefit of shareholders.

Finally, the ethical-normative approach represents the desired evolution of the confluence of the three analyzed conceptual axes, laying its foundation on a business concept whose management is oriented to the common good, considering effectively the interests, desires and goals of all those who somehow they affect the company or are affected by it. As expressed Cortina (1994/2000), it is an approach in which business ethics is not rhetoric, but is applied ethics. This approach, according Cortina (2003), draws on ideas consistent outsold the need that contemporary societies found that beliefs, convictions and ethical habits are essential for the proper functioning of the business world.

The ethical-normative approach is a step beyond raising the strategic-instrumental approach, proposing a model of inclusive company, in which each group of stakeholders deserves consideration so that in itself represents and not only for its capacity to be a means or instrument of another group to consider stakeholders as human beings, by nature complex, begin to place ethics and responsibility at the heart of a new way of thinking businesses. According to Rodriguez Fernandez (2007) this business model entails undoubtedly strict compliance with the laws, but also respect for human rights, ethical behavior, fair competition and environmental care.

CONCLUSION

This bibliographical research about the three conceptual pillars on which today companies articulate their actions socially and environmentally responsible showed, that despite these concepts are born businesswoman consideration in different times and circumstances. Different orientations and focused on aspects many, in the present times converge and are integrated into a set of ideas that define the design and strategies of those companies that choose to manage superseders criteria for pure equity model.

The work also showed how the concepts of CSR and stakeholder theory presented in the doctrine as essentially controversial-not so that of sustainability-enabling companies to make applications idiosyncratic them in their efforts. Also, considering that currently the prevailing concept as guiding shares in companies is sustainability, it is striking that excessive use is made of the concept of the term especially himself within it including aspects that were always in consideration entrepreneur but who now they are sustainable adjective adosa.

Based on these considerations, and in order to have an adequate tool for evaluating business actions beyond definitions and names that companies awarded them a scheme Galbreath (2006) was adapted with the intention of putting the accent on the theoretical foundation that guides every business performance. This tool can not only be useful to look at the reality of women entrepreneurs performances with possibilities of greater detail and differentiation, but also applies to help frame and adjustment of the various doctrinal contributions, activity that exceeds the objectives of this work.

And back to the metaphor of the puzzle as an expression of CSR, it is likely that for a while it still can not assemble more than their edges. But it is clear that day after day are incorporated into it more content and more concepts, making impossible a single resolution because its parts are in continuous reconfiguration.

But beyond the academic and professional concern that anyone can have on these issues, ultimately the essence of his study should concentrate on trying to ascertain whether the foundation is located at the confluence of the three themes discussed -RSE, sustainability and stakeholders- necessary for companies to evolve in a way to be more company sincerely committed to social and environmental, or if these concepts, as posed Argandoña (2007), with the passage of time are at risk of becoming a more administrative fashions.

Depending on the evolution, interaction, interaction and mutual taxation that had the three constructs analyzed and beyond the differentiation may be made of the concepts and definitions, it is conceivable that currently is being written an important chapter in shaping of a single theory that encompasses all these concepts plus some others that will be refined in the future. Somehow, and as happens in theoretical physics that is years after the search of the Theory of Everything-called M-theory, one that allows both explain what happens at astronomical scales as what happens to cuántico- level the field of business management can hypothesize that all these different conceptual aspects of responsible and sustainable management are amalgamated into a single body of ideas whose aim is to generate more ethical, transparent and greater social commitment entrepreneurs efforts and environmental, conception rooted in a larger number of companies every day.

A survey on the concepts analyzed allows viewing amalgamated into a unified theory, a conceptual body in which the entrepreneur rationality coexist harmoniously self-interest and the interest of others, morality and guidelines efficient performance. One theory on which companies can base their actions, and where ethics and business are concepts that do not go our separate ways, but part of that one entrepreneur rationality.

Within this prospective vision it can be thought that some terms CSR, sustainability and stakeholders will be relegated, generating new debates about the proper name should be the prevailing theoretical approach. Within this vision of the future perhaps soon to be finalized names like BioGestión, or government eco-responsible business, management or biodynamic, or sustainable holistic management, or biokinetic biotópico government and organizations. In any case, and as previously stated, it is bounded in the field of academic and doctrinal debate, and ultimately will be the companies that with their actions, configure the future.

Notes

* Among the initials United Nations Conference on Environment and Development, Stockholm, Sweden, 1792; the document World Conservation Strategy prepared by the International Union for Conservation of Nature, the United Nations Environment Programme, the World Wide Fund for Nature, and UNESCO, 1980; the World Charter for Nature, adopted by the UN, 1982; in 1983 the UN General Assembly created the World Commission on Environment and Development.

**“15 Beware of false prophets, which come to you in sheep's clothing, but inwardly are ravenous wolves. 16 By their fruits ye shall know them. Do men gather grapes of thorns, or figs from thistles? 17 Even so every good tree bears good fruit, but a bad tree bears bad fruit. 18 A good tree can not bear bad fruit, nor can a bad tree bear good fruit” (Mateo 7:15-20, Sociedades Bíblicas en América Latina, p. 881).

*** Only just read the reports about these actions by the companies.

BIBLIOGRAPHICAL ABSTRACT

Please refer to articles Spanish Bibliographical Abstract.

REFERENCES

Please refer to articles in Spanish References.